Brian Foster grips the pen over a

0:00 / 1:00

60-second animated preview

Watch full summaryThe Millionaire Next Door Summary

What is The Millionaire Next Door about?

The Millionaire Next Door by Thomas J. Stanley and William D. Danko reveals that most real millionaires live surprisingly modestly, and it shows how ordinary earners can quietly build lasting wealth.

Book details

- Author

- Thomas J. Stanley and William D. Danko

- Reading time

- 10 min read

- Topics

- Not mapped yet

Main ideas at a glance

3 visualsAre You a PAW or a UAW?

Big Hat, No Cattle vs. The Quiet Millionaire

The Millionaire Next Door Summary

Brian Foster grips the pen over a lease agreement for a brand new BMW, determined to finally look successful, while his phone buzzes with a low-balance alert from his bank.

(Continued below)

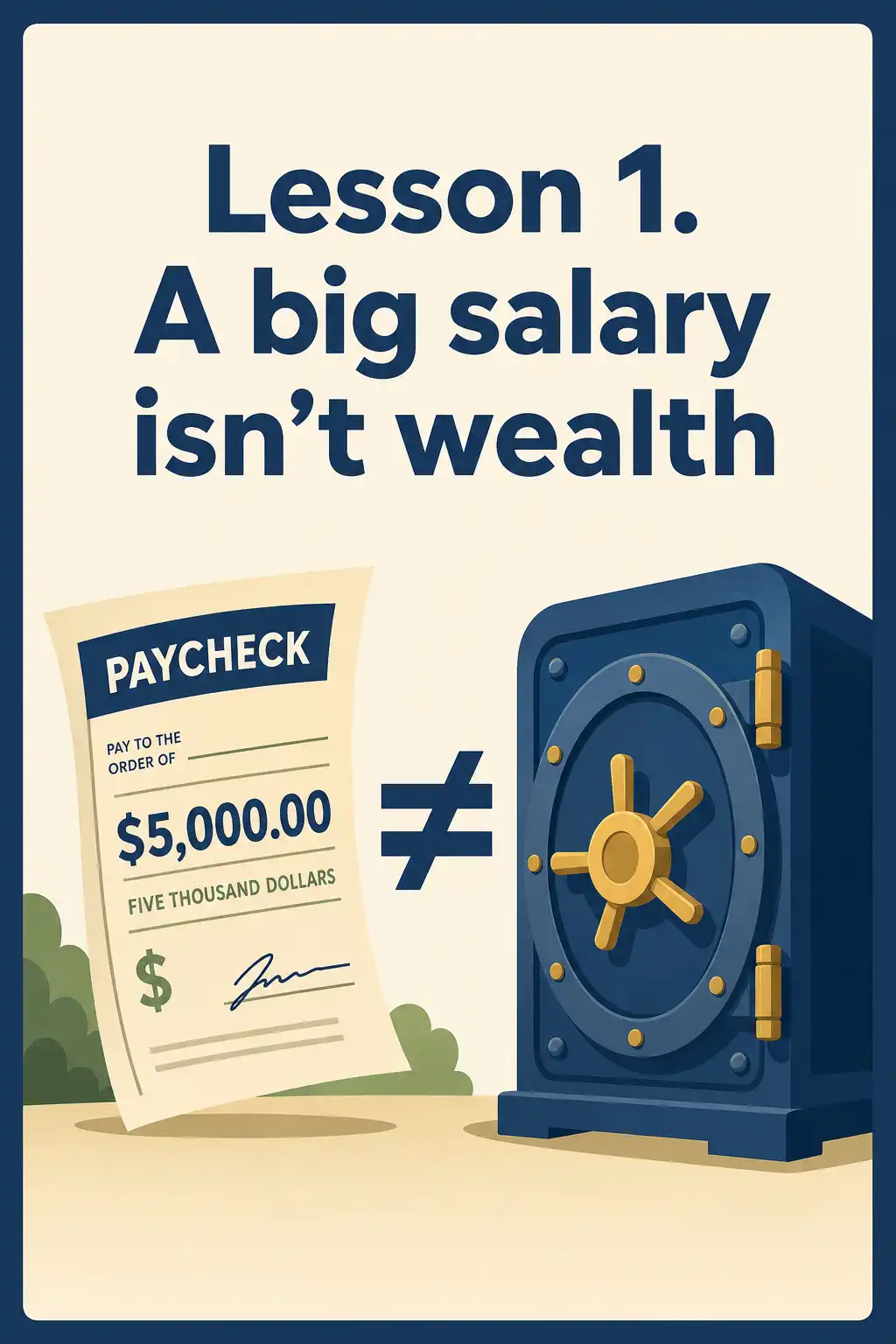

1. A big salary isn't wealth

Brian signs the lease anyway, drives home in the BMW, and feels great for exactly two days. Then he sits down to file his taxes that weekend, and the buzz wears off fast.

He's 38, a territory sales manager for a commercial HVAC distributor in Savannah. He earns $140,000 a year. And yet, his savings would barely cover two months of bills.

That night he stumbles onto research by Thomas Stanley and William Danko, two academics who surveyed thousands of American millionaires and interviewed over five hundred of them face to face.

Their surprising discovery? Many people in expensive homes with luxury cars have almost no actual wealth, while many true millionaires live quietly in ordinary, modest neighborhoods. In fact, the authors found millionaires clustered in middle-class and blue-collar neighborhoods, not the fancy ones.

The key idea hits Brian hard. Income and wealth aren't the same thing. A high salary means nothing if every dollar of it gets spent.

Real wealth is what you keep and accumulate. Most Americans, even high earners, live paycheck to paycheck, with household net worth near zero once you take away their home.

2. Big hat, no cattle

Monday morning, Brian visits a client named Ray, who owns a paving company. Ray wears jeans, drives a ten-year-old pickup, and casually mentions he just paid cash for a rental property.

Brian is stunned. Ray looks like a truck driver but is worth millions. Stanley and Danko have a colorful Texas expression for the opposite kind of person. Big hat, no cattle.

In their research, a bank trust officer once dined with ten first-generation millionaires and insisted they couldn't possibly be wealthy, simply because they didn't look the part.

The irony? That officer wore a five-thousand-dollar watch and leased a luxury car while quietly spending himself broke. The modest millionaires he dismissed had the actual cattle.

The authors offer a simple test. Multiply your age by your pretax annual income, then divide by ten. That, roughly speaking, is what your net worth should be.

Brian does the math. 38 times 140,000, divided by ten, is $532,000. His actual net worth? About $45,000. That makes him what the authors call an under accumulator of wealth.

3. Frugal, frugal, frugal

That evening, Brian and his wife Jenna pull up their credit card statements together. Restaurants, clothes, subscriptions. Neither of them can honestly say what they spend in a typical month.

According to Stanley and Danko, frugality is the cornerstone of wealth. Half the millionaires they surveyed had never spent more than $399 on a suit in their entire lives.

In one famous story from the book, a millionaire's wife received eight million dollars in company stock one afternoon, smiled, and went right back to clipping grocery coupons at the kitchen table.

The authors pose four questions. Do you budget? Do you know what you spend on food, clothing, and shelter? Do you have clear goals? And do you plan your financial future?

Most millionaires answer yes to all four. Brian and Jenna can't answer yes to any of them. So that night, they sit down and build their first real household budget together.

They also adopt the authors' pay-yourself-first shortcut: invest at least fifteen percent of your income before spending anything else. It creates a kind of artificial scarcity, forcing discipline on whatever remains.

4. Spend time, not just money

A few months in, Brian notices something odd about himself. He spent twelve hours last year researching a new TV, and zero hours researching his own retirement investments.

Stanley and Danko describe two doctors with identical $700,000 incomes. Dr. North built $7.5 million in wealth. Dr. South, despite the exact same earnings, had only $400,000 to show for it.

Dr. South once spent sixty hours negotiating a Porsche purchase, while contributing almost nothing to his pension. Dr. North spent those same hours studying investments instead.

The pattern holds broadly. Wealth builders spend nearly twice as many hours per month planning their investments as under accumulators do. Where attention goes, money grows.

Millionaires also aren't frantic day traders. Most hold their investments for years, and over forty percent made no stock trades at all in a given year. Patience compounds quietly.

So Brian blocks two hours every Sunday for financial planning. He finds a good CPA first, then asks her to refer a trustworthy investment advisor, just as the book suggests.

5. Your home sets your overhead

That spring, Jenna finds a gorgeous listing in Savannah's most prestigious neighborhood. Their realtor insists they can qualify for the mortgage. And technically, that's true.

But Brian remembers the authors' rule. Never take a mortgage bigger than twice your household's annual income. This one would be nearly four times theirs.

The deeper problem isn't just the monthly payment. Expensive neighborhoods pressure you into expensive everything. The landscaping, the cars, the private schools, the vacations that have to match the neighbors'.

Stanley and Danko found that people who buy status homes hoping the wealth will follow usually never get there. Their overhead quietly consumes everything they might have invested.

Millionaires typically do it backwards. They accumulate wealth first, in modest homes they've often owned for over twenty years, and only then upgrade, if it still makes sense.

Brian and Jenna stay in their current house. The money that would have gone toward the bigger mortgage flows into index funds and retirement accounts instead.

6. Buy your cars by the pound

When Brian's BMW lease finally ends, he stands in the dealership again, right where this whole story started. This time, he walks out without signing anything.

The data changed his mind. Most millionaires buy their cars rather than lease, and over a third buy used. Half never spent more than $29,000 on any vehicle, ever.

Stanley and Danko say millionaires buy cars by the pound. A big domestic sedan delivers far more car per dollar than a luxury import costing three times as much.

The savviest group of all, the used-car bargain hunters, had the lowest incomes of any millionaire type in the study. Yet they still averaged over three million dollars in net worth.

Their secret is letting someone else absorb the depreciation. A two or three-year-old car has already taken its steepest drop in value, but it works just as well.

Brian buys a three-year-old Ford for a fraction of the BMW's cost, and he pays cash. Ray, his paving client, nods approvingly from his ten-year-old pickup.

7. Beware economic outpatient care

That summer, Brian's parents offer to help out with a check, like they've quietly been doing for his younger brother Kyle for years. Brian hesitates.

Kyle earns good money as an attorney, and yet he lives paycheck to paycheck in an upscale neighborhood, floated by their parents' regular gifts. The book saw this exact scenario coming.

Stanley and Danko call it economic outpatient care. Ongoing cash support from affluent parents to their adult children. And nearly half of affluent parents give it.

The results are deeply counterintuitive. In almost every profession studied, adults who receive parental cash accumulate significantly less wealth than those who receive nothing at all.

Why? Because the gifts push recipients into lifestyles their own incomes can't sustain. They spend more, borrow more, invest less, and feel wealthier than they actually are.

Brian politely declines the check and asks his parents to put the money toward the grandkids' education instead. The authors endorse funding education, not consumption.

8. Play offense with your career

Two years later, Jenna, a CPA at a big firm, notices something on her client list. Her wealthiest clients are business owners in gloriously boring industries.

That matches the research exactly. Self-employed people are only about a fifth of American workers, yet they're four times more likely to become millionaires than employees.

And the businesses are rarely glamorous. Pest control, paving, janitorial services, mobile-home parks. Dull-normal industries quietly build fortunes while attracting little competition or attention.

The authors also point out that serving the affluent is itself a great niche. Wealthy families spend freely on professional services, especially tax and estate planning.

So Jenna launches her own accounting practice serving small business owners like Ray. Within eighteen months, she's earning more than her old salary, with plenty of room to grow.

Five years after that overdraft alert, Brian and Jenna's net worth crosses $500,000 and keeps climbing. They're on pace to reach the PAW column well before fifty.

Next step

Want the animated version?

Quick setup, then watch this summary in a more engaging visual format.