Lesson 1: Why index funds win

Laura sets the glossy brochure down. A colleague swore this actively managed tech fund would crush the market. But is paying experts to pick stocks really worth it?

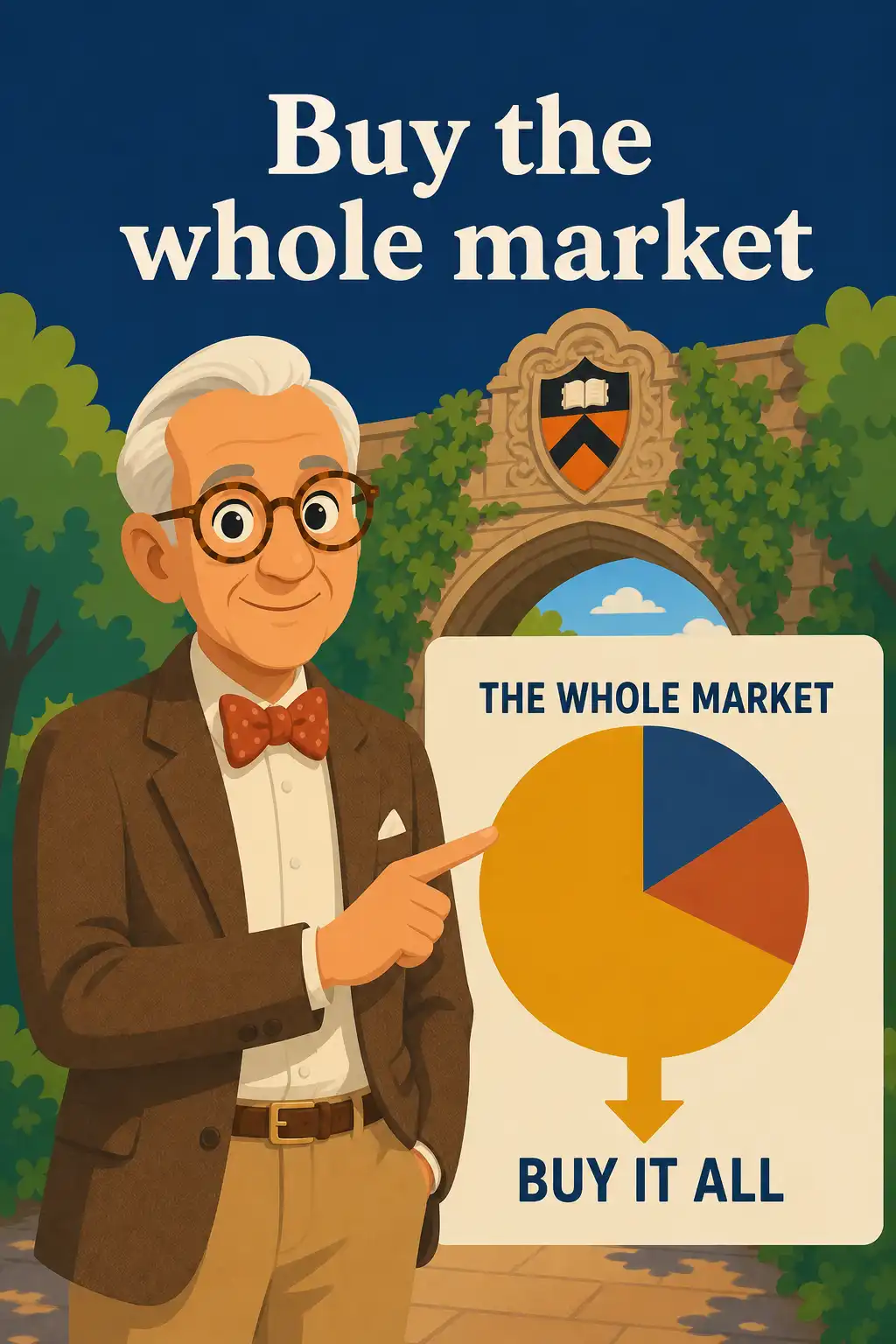

Burton Malkiel, a Princeton economist, has spent decades wrestling with this exact question. His answer is blunt. Most investors do far better simply buying a fund that mirrors the entire market.

An index fund just holds every stock in a broad basket, like the S&P 500, which tracks five hundred big U.S. companies. No stock picking. Tiny fees.

Malkiel shares a stunning comparison. Two people each invested ten thousand dollars back in 1969. By 2014, the one holding a simple index fund had over seven hundred thousand dollars.

The one paying for the average active fund? Just five hundred thousand. That gap, nearly a quarter million dollars, was eaten up mostly by higher fees.

Laura does the math. Every dollar skimmed by a manager is a dollar not compounding for her retirement. Suddenly that hot fund looks a lot less appealing.