A detailed summary ofThe Psychology of Moneyby Morgan Housel

The Psychology of Money by Morgan Housel argues that doing well with money has less to do with intelligence and more with behavior.

Wedged into a folding chair at her

0:00 / 1:00

60-second animated preview

Summary Visuals

Getting Wealthy vs. Staying Wealthy

The Quiet Path to Wealth

The Psychology of Money Summary

Wedged into a folding chair at her cousin's backyard barbecue, Rebecca Hartley overhears bragging about crypto wins and feels her stomach tighten with quiet panic.

1. Behavior beats brilliance

Rebecca is a thirty-four-year-old dental hygienist in Tacoma, Washington. She earns a decent living, but her savings account barely budges from month to month.

At the barbecue, her cousin Tyler keeps name-dropping hot stocks. Rebecca nods along, secretly wondering why smart-sounding people seem to be racing ahead of her.

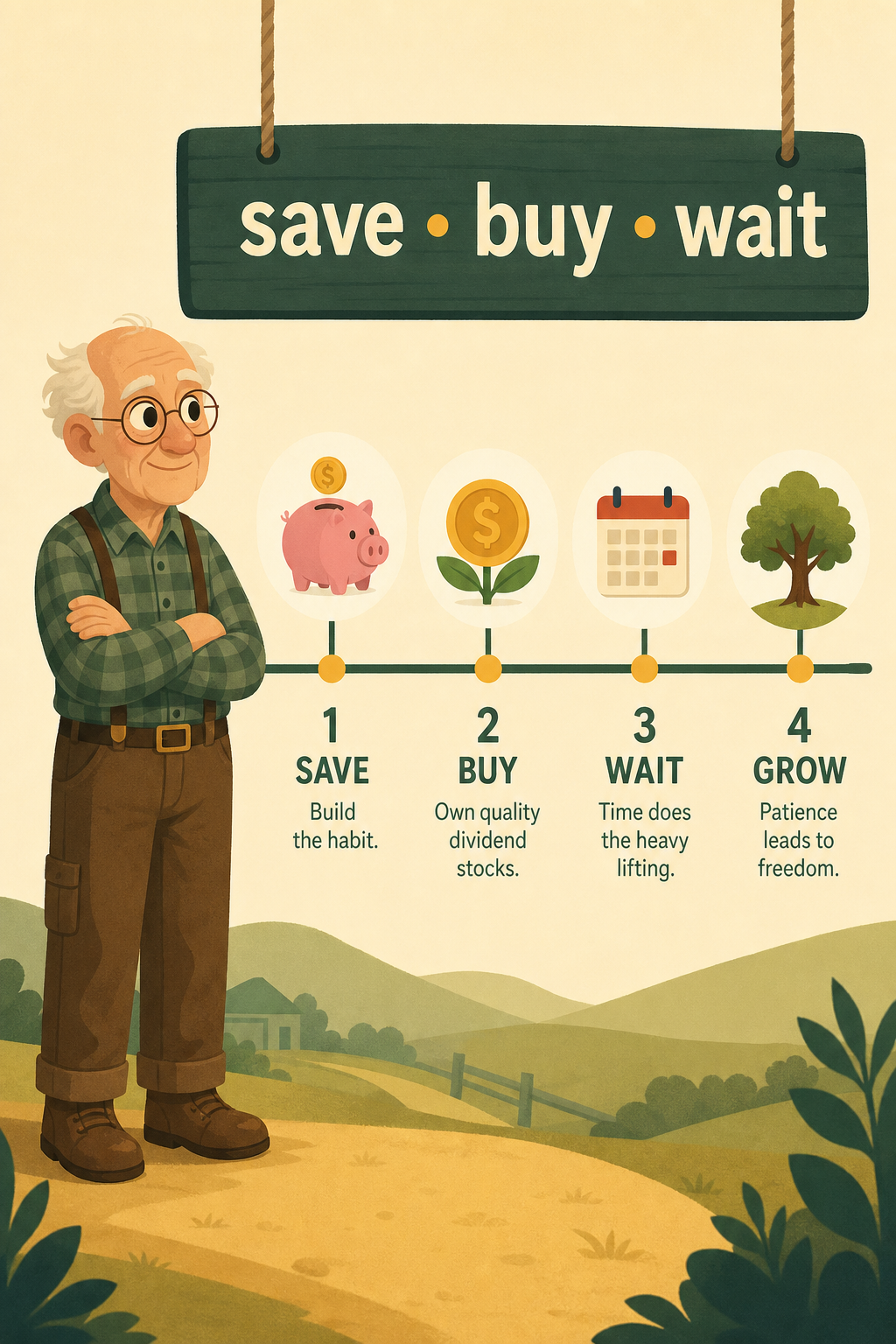

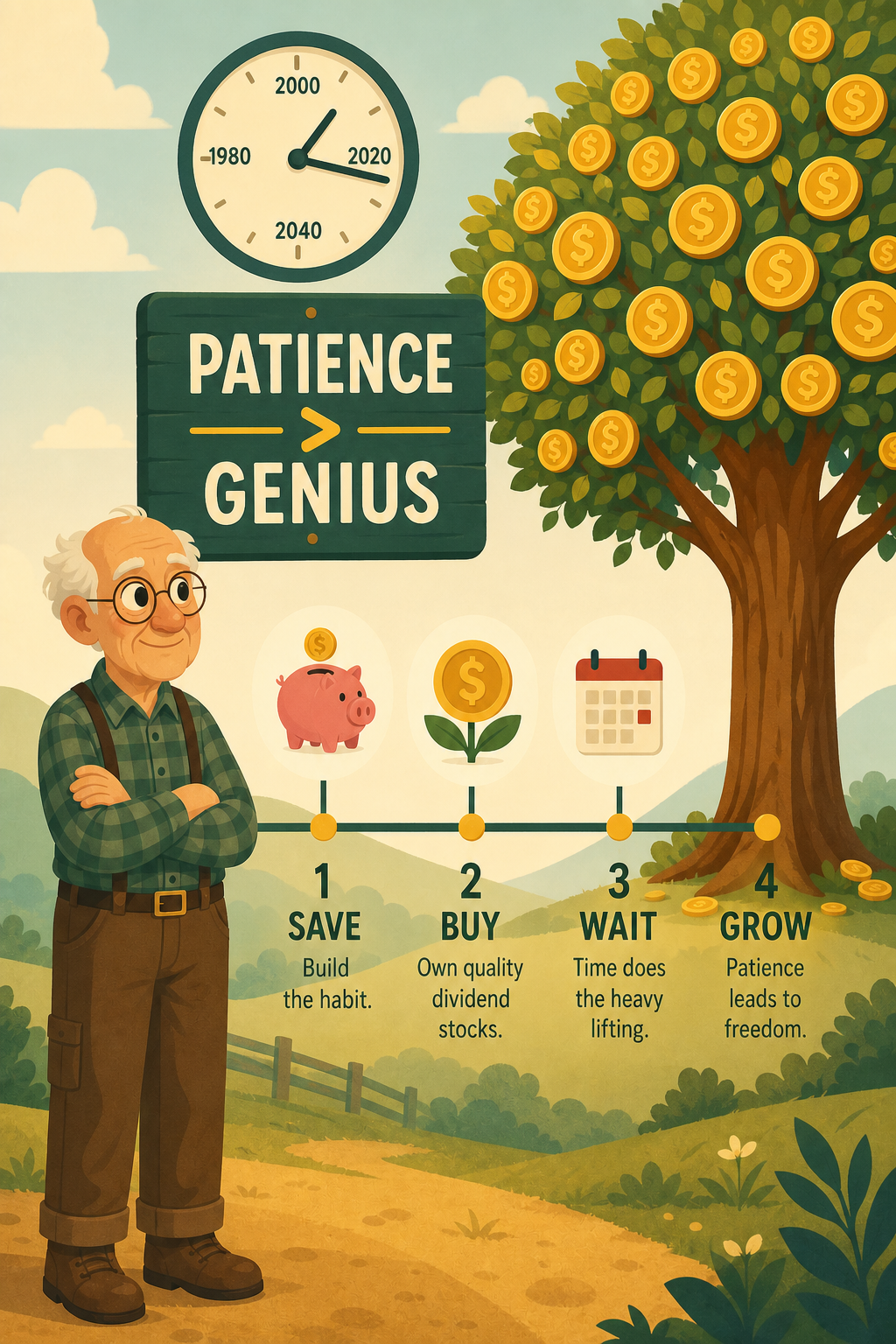

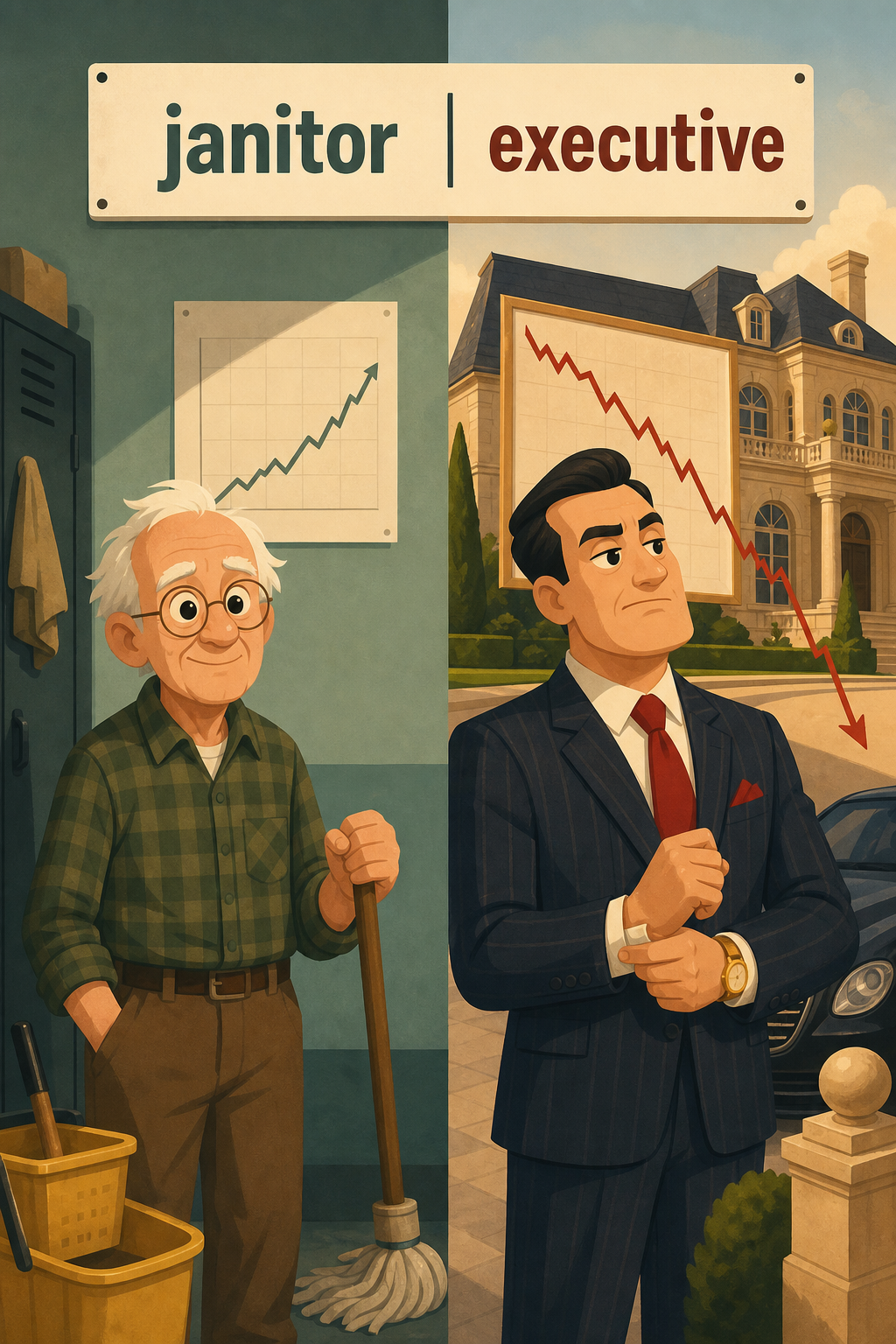

That night, she remembers a story Morgan Housel tells about Ronald Read, a Vermont janitor who quietly left behind nearly eight million dollars when he died.

Read never went to business school. He just saved, bought solid dividend-paying stocks, and waited decades. His secret was patience, not genius.

Housel contrasts him with Richard Fuscone, a Harvard-trained finance executive who borrowed heavily, lived large, and lost everything in the 2008 crash.

Rebecca sees herself somewhere in the middle. She's not a janitor or an executive, but she has been measuring herself by the wrong yardstick entirely.

Next step

Watch The Psychology of Money instead

Quick setup, then watch this summary in a more engaging visual format.

iOS + Android app20,000+ learnersFree daily summary

2. Nobody is crazy

A week later, Rebecca watches a coworker buying lottery tickets on payday. Her first thought is judgmental. Her second thought stops her cold.

Housel points out that lower-income households spend dramatically more on lottery tickets than wealthier ones. From the outside, that looks irrational and self-defeating.

But Housel argues these choices make perfect sense from inside someone's life. A lottery ticket might be the only tangible dream of escape someone has.

Everyone's money decisions are shaped by the era they grew up in, their parents, their paychecks, and what they personally lived through.

Rebecca's mom lived through the early eighties recession and still hides cash in coffee cans. That isn't crazy. It's a scar from real experience.

Housel also notes how new our financial tools really are. The 401(k) only appeared in 1978, and the Roth IRA didn't show up until 1998.

3. Luck and risk are twins

At work, a senior hygienist brags about buying Apple stock back in 2009. Rebecca almost feels embarrassed, then remembers another story from Housel.

Bill Gates attended Lakeside School in 1968, one of the only high schools in the world with a computer at the time. Roughly one in a million odds.

His best friend Kent Evans had the same talent and the same access, but was killed in a mountaineering accident before graduation. Same odds, opposite direction.

Housel says luck and risk are siblings. Both shape outcomes far more than effort alone, but we rarely give either its proper weight.

Rebecca decides not to envy her coworker's lucky bet, and not to beat herself up for missing it. Neither response would teach her anything useful.

Instead, she focuses on broad patterns. Steady savers tend to do well over time. Reckless gamblers occasionally win big and often lose everything.

4. Knowing when enough is enough

Rebecca gets a small raise and immediately starts browsing newer cars online. Her current Honda runs fine, but somehow it suddenly feels embarrassing.

She catches herself and thinks of Housel's story about Rajat Gupta, who rose from poverty in India to become a McKinsey CEO worth around a hundred million dollars.

Gupta wanted billionaire status, leaked insider tips to a hedge fund manager, and ended up convicted and sent to prison. He already had more than enough.

Housel warns about moving goalposts. When your definition of enough keeps sliding upward, you take bigger risks chasing a finish line that never actually arrives.

Social comparison, he says, is a game nobody wins. There will always be a fancier car parked next to yours.

Rebecca closes the browser tab. Her reputation, her freedom, her sleep at night, these are things no upgrade is worth gambling.

5. Let compounding do the work

Rebecca finally opens a Roth IRA and stares at the modest monthly contribution she can afford. It feels almost pointlessly small.

Then she remembers Housel's wild fact. The vast majority of Warren Buffett's fortune was accumulated long after his sixty-fifth birthday.

Buffett's real edge isn't picking magical stocks. It's that he started investing as a kid and simply never stopped for over seven decades.

Housel compares compounding to an ice age. Small leftover patches of snow, repeated year after year, slowly built continent-sized ice sheets.

Our brains think in straight lines, not exponential curves. So we constantly underestimate what tiny, boring contributions can become over thirty or forty years.

Rebecca recalculates with patience instead of panic. Modest contributions, left untouched for decades, could quietly grow into something life-changing.

6. Getting wealthy versus staying wealthy

A patient mentions he just refinanced his house to buy more tech stocks. Rebecca tries to sound polite, but inwardly she winces.

Housel tells the story of Jesse Livermore, who made roughly a hundred million dollars shorting the market during the 1929 crash, then lost it all within a few years.

Getting rich and staying rich, Housel says, take opposite mindsets. Building wealth needs optimism. Keeping wealth needs humility and a healthy fear of losing it.

Buffett's real genius isn't just great picks. It's that he never used dangerous debt, never panicked in a downturn, and never quit the game.

Rebecca decides survival comes first. She keeps an emergency fund even though it earns almost nothing, because cash means she'll never be a forced seller.

She builds a margin of safety into her plan. If her car dies or her hours get cut, she won't have to unravel her investments at the worst possible time.

7. Tails drive everything

Rebecca's friend laughs at her boring index fund. Why settle for average, she asks, when you could pick the next big winner?

Housel shares data from the Russell 3000 index. Forty percent of those companies suffered catastrophic losses over time, yet the overall index rose more than seventy-three-fold.

Just seven percent of companies drove almost all the gains. Most stocks were duds. A tiny handful were spectacular tail events.

Art dealer Heinz Berggruen built a legendary collection by buying enormous quantities of work and holding long enough for a few masterpieces by Picasso and Klee to define his legacy.

Rebecca realizes her index fund already owns those rare winners automatically. She doesn't need to guess which company will be the next Amazon.

Housel's takeaway is freeing. Being wrong often is completely normal. What matters is being positioned so a few big wins more than cover everything else.

8. Time is the real prize

Rebecca's clinic offers her overtime that would pay nicely but cost her every Saturday. A year ago, she would have said yes immediately.

Housel points to research showing that a sense of control over your own time predicts happiness better than income, education, or location.

Cornell gerontologist Karl Pillemer interviewed roughly a thousand elderly Americans about what truly mattered. Not one wished they'd worked harder to earn more money.

They valued relationships, purpose, and unhurried time with the people they loved. The highest dividend money can pay is control over your own schedule.

Rebecca declines the overtime. She uses Saturday to visit her mom and finally start the pottery class she's been postponing for two years.

She also stops envying flashy spenders. Housel notes that nobody actually admires the owner of the fancy car. People just imagine themselves driving it.

9. Wealth is what you don't see

At a coworker's housewarming, Rebecca tours a beautiful home and wonders how anyone affords it. Then she remembers Housel's blunt distinction.

Rich means high income, often visible through spending. Wealth means money not yet spent, quietly stored as savings, investments, and future options.

A fancy car only tells you someone has less money than they did before they bought it. True wealth, by its very nature, is invisible.

Housel's prescription is simple. Save aggressively, especially without a specific goal in mind, because that buffer buys flexibility, freedom, and clear thinking when life surprises you.

Rebecca starts treating market volatility as a fee, not a fine. The discomfort of watching her balance dip is just the price of admission for long-term growth.

She knows her game now. She's not a day trader or a billionaire. She's Rebecca Hartley, building quiet independence one steady paycheck at a time.

Next step

Start watching in minutes

Take the short quiz and unlock animated summaries you can watch or listen to daily.

iOS + Android app20,000+ learnersFree daily summary

More books like The Psychology of Money

I Will Teach You to Be Rich

by Ramit Sethi

"I Will Teach You to Be Rich" by Ramit Sethi lays out a step-by-step system for automating your money, so you can spend guilt-free on the things you actually love.

The Millionaire Next Door

by Thomas J. Stanley and William D. Danko

The Millionaire Next Door by Thomas J. Stanley and William D. Danko reveals that most real millionaires live surprisingly modestly, and it shows how ordinary earners can quietly build lasting wealth.

The Book on Rental Property Investing

by Brandon Turner

The Book on Rental Property Investing by Brandon Turner is a practical guide to building lasting wealth and financial freedom by buying, managing, and growing a portfolio of rental properties.

A Random Walk Down Wall Street

by Burton G. Malkiel

A Random Walk Down Wall Street by Burton G. Malkiel makes a bold argument. Ordinary investors do best by ignoring hot tips and simply buying and holding low-cost index funds for the long haul.

Rich Dad Poor Dad

by Robert Kiyosaki

Rich Dad Poor Dad by Robert Kiyosaki is a book about how the wealthy think differently about money, and how anyone, no matter where they start, can learn to play by their rules.

The Richest Man in Babylon

by George S. Clason

"The Richest Man in Babylon" by George S. Clason uses ancient parables to teach timeless principles of saving, investing, and growing your money.

Related book lists

12 summaries

Money

Master earning, saving, and building financial freedom.

7 summaries

Personal Finance

Managing money including saving spending investing and budgeting.

10 summaries

Investing

Grow wealth strategically through markets, mindset, and compounding.

17 summaries

Bestseller

Widely read, highly rated books people are loving right now.