Lesson 1: Stop debating and start doing

Picture someone who reads every fitness article online and debates protein powders for months, but never actually sets foot inside a gym. That's most people with money.

Ramit Sethi noticed this pattern everywhere. People obsess over tiny financial details while completely ignoring the simple steps that actually build wealth over time.

Sethi is a Stanford graduate and personal finance author. He built a six-week program around one core idea: take action now, even if it's imperfect.

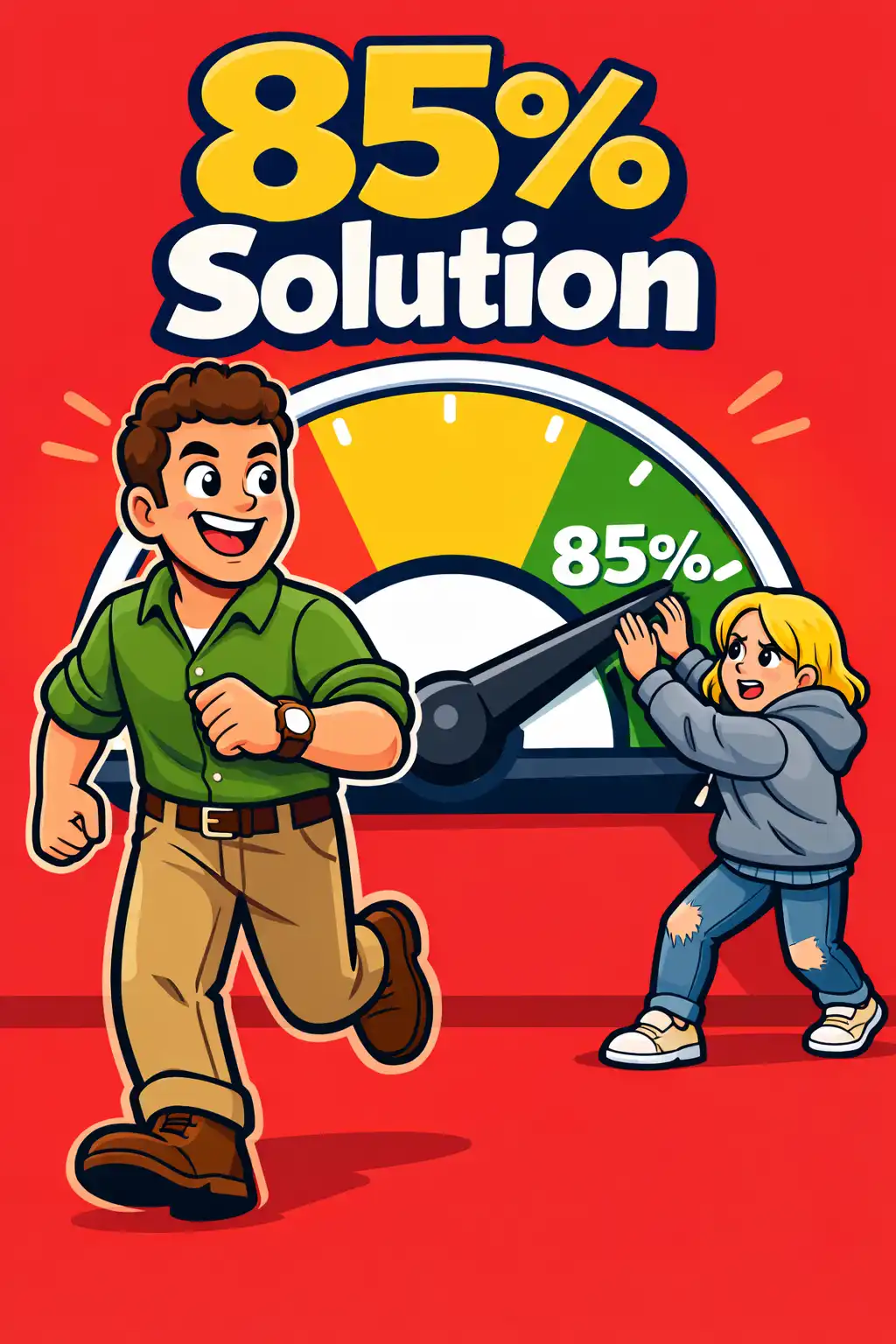

He calls this the "85 Percent Solution." Getting it mostly right and moving forward will always beat endlessly researching the perfect plan you never follow.

Here's the real cost of waiting. Someone who invests two hundred dollars a month starting at age twenty-five ends up with far more than someone who starts at thirty-five with double the amount.

That's because compound interest rewards early starters massively. The math is unforgiving. Every single year you delay costs you more than you think.