Lesson 1: Investing is about discipline, not genius

Picture a young boy growing up in poverty. His father has just died, and his mother has lost everything in the devastating financial panic of 1907.

That boy was Benjamin Graham. Despite those beginnings, he went on to build one of the most successful and respected careers Wall Street has ever seen.

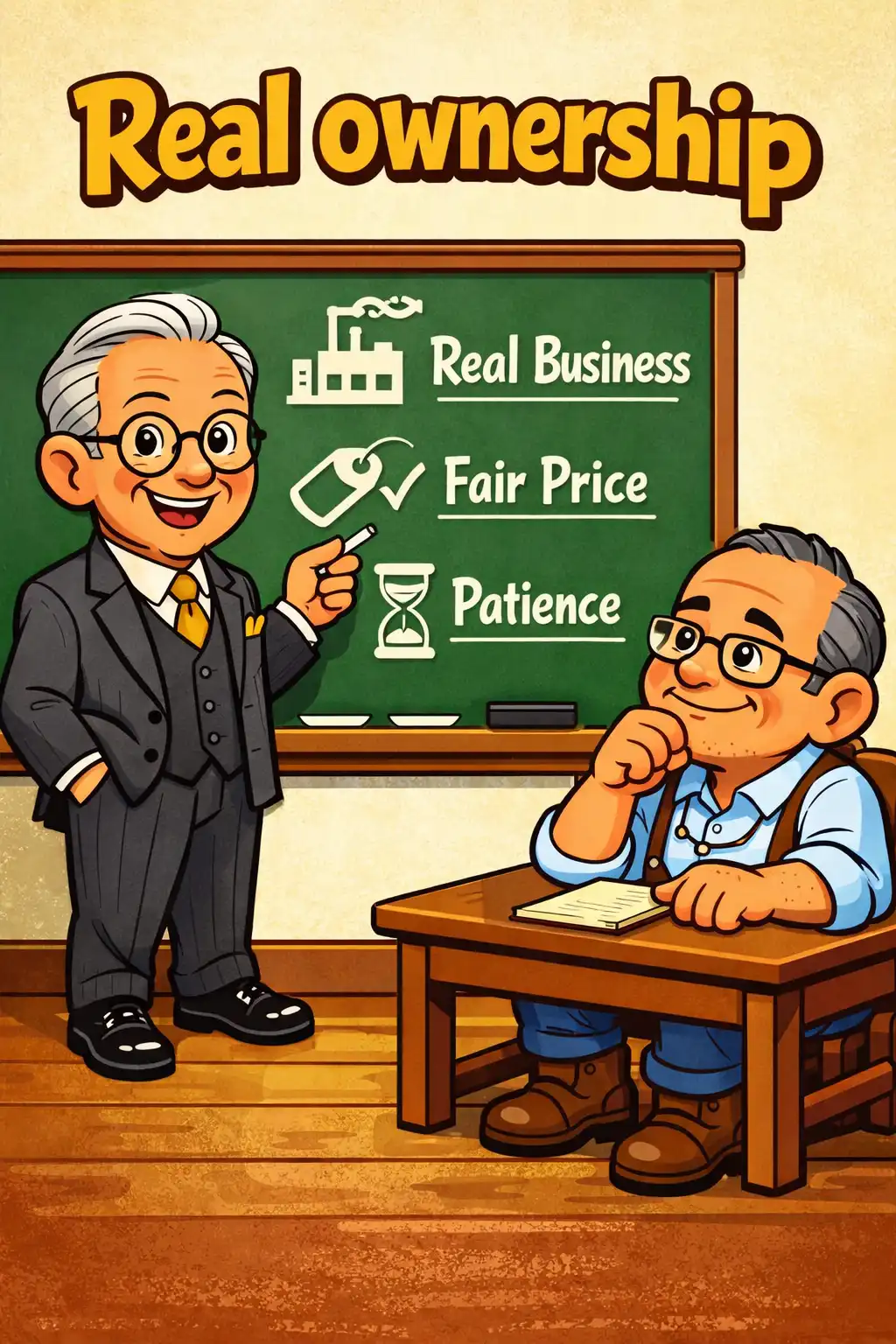

Graham's core teaching was surprisingly simple. Treat stocks as real ownership in real businesses. Never overpay. And let patience guide every single decision you make.

His most famous student, Warren Buffett, called this the best book on investing ever written. Not because it promises quick riches, but for a deeper reason.

It gives you a framework for thinking clearly when everyone else is panicking. Graham believed successful investing requires emotional discipline, not a high IQ.